Zurich Climate Week 2026 brought together senior sustainability leaders, investors, and financial institutions to address the future of carbon markets, climate finance, and credible net zero strategies. Across four sessions attended plus countless meetings held between 5 and 7 May, one message cut through consistently: the market has moved past intention. Execution is now the measure of credibility.

Here are the key takeaways shaping how companies move from ambition to implementation.

1. Policy clarity remains the single biggest blocker

Across every session, from carbon dioxide removal to energy transition, regulatory uncertainty was cited as the primary reason companies are not moving faster. Most corporates are positioning themselves as followers, waiting for policy frameworks before committing capital or making public commitments.

The problem is structural: markets want certainty before acting, but certainty only comes once early movers have created it. This is not a comfort zone; it is a competitive risk. Companies that fail to engage now will face higher compliance costs and less favourable terms as regulation tightens.

For carbon markets specifically, the CDR session was unambiguous: waiting is not a neutral position. The cost of delay now exceeds the cost of imperfect action.

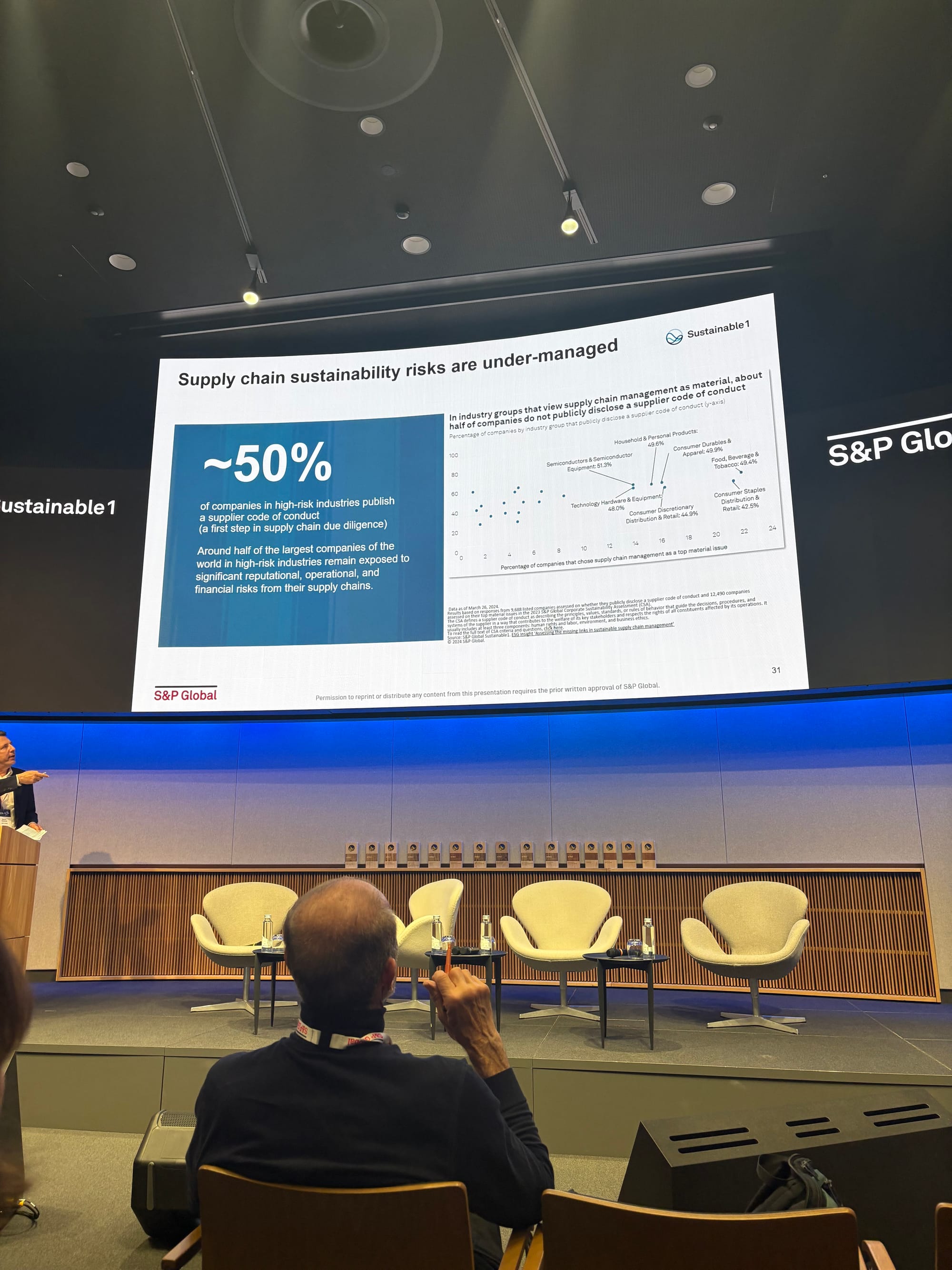

2. Measurement and disclosure are becoming the new standard of credibility

The S&P Global Sustainability Yearbook session made the market's direction clear: only commitments that are public get measured, and only what gets measured carries commercial weight. High-level net zero pledges are no longer sufficient. Clients, and increasingly regulators, are demanding granular detail, particularly on Scope 3 and supply chain accountability.

58% of companies in corporate supply chains already have sustainability guidelines in place. The other 42% represents both a risk concentration and an engagement opportunity. CSA scores are emerging as a useful signal for identifying where compliance behaviour is heading before it becomes a formal obligation.

3. Capital is available. Bankable structures are not.

The UBS Innovating for Nature session reframed nature from a moral issue to a systemic financial risk: 50% of global GDP is estimated to depend on ecosystem services. 38% of Swiss rivers are already polluted. These are not soft statistics, they carry reputational and balance sheet weight.

The funding is not the problem. Trillions are available. The bottleneck is the absence of investable structures that bridge the gap between corporate annual reporting cycles and the 10 to 30 year timelines required for meaningful nature and climate outcomes.

Outcome bonds, insetting models, and bio asset bonds are gaining traction as the mechanisms most likely to resolve this mismatch. The Amazon bio asset bond, managed through Optimus’ $100m impact fund, was cited as a working example of how blended structures can deliver annual reporting-compatible returns alongside long-term impact.

4. Voluntary and compliance markets are converging

The Green Fintech CDR session noted positive signals on convergence between voluntary carbon markets and compliance frameworks. Market integrity is improving. Collaboration across the value chain is increasing. The technology question for CDR is largely resolved, multiple pathways now exist.

What remains is the willingness to act ahead of policy, rather than after it. The companies that build CDR procurement strategies now will be better positioned when compliance requirements formalise, both in terms of cost and in terms of the quality of credits available to them.

5. Energy transition requires more than incremental improvement

The UBS Energy Transition session was clear that the pace of change required is not compatible with marginal improvements to existing infrastructure. New technology, significant capital reallocation, and grid expansion are all prerequisites, not optional accelerants.

Modular nuclear is emerging as a viable part of the mix. A US programme (DOW model) is producing factory-built modules deployed on site, reducing construction risk and capital expenditure significantly. European applicability is under active discussion. Grid digitalisation and public acceptance were both flagged as under-priced risk factors in transition portfolios.

What this means for carbon markets

Zurich reinforced what Carbonaires sees consistently across the market: the infrastructure for credible climate action is forming faster than corporate decision-making is keeping pace with it.

Demand for high-quality carbon credits is shifting from aspirational to structural. Buyers are prioritising integrity, verification and removal-based credits, and the pool of credible supply is not growing fast enough to meet the demand that is coming once compliance integration and disclosure requirements fully bite. The pricing implications of that gap are significant for companies that have not yet secured supply. Early offtake agreements are already delivering better terms and better access to quality projects. That advantage compounds over time.

The capital markets story is moving in the same direction. Institutional investors are not waiting for perfect policy conditions. They are building the financing vehicles and long-dated instruments that will define how climate investment scales through the back half of this decade. The emergence of bio asset bonds and insetting models is not peripheral to the carbon market story. It is part of the same structural shift toward investment-grade climate finance that will reshape how carbon removal is sourced, financed and reported.

The convergence of voluntary and compliance markets adds further urgency. Companies still operating without a structured carbon procurement strategy will find themselves competing for a smaller pool of credible credits at higher cost, and with less time to build the internal governance required to deploy them credibly. The organisations that move now are not taking a risk. They are managing one.

This is where structured approaches and platforms like Carbonaires support faster, more credible decision-making in carbon markets, carbon removal and wider corporate decarbonisation strategy.

Carbonaires perspective

At Carbonaires, we see three clear shifts emerging from Zurich.

First, the market is moving from ambition to accountability. Public disclosure is no longer optional. The market now assumes that what is not disclosed does not exist. Companies need governance structures that embed sustainability into decision-making, not reporting processes that bolt it on afterwards.

Second, the shift from following to leading is becoming a commercial imperative, not just a strategic preference. The follower posture that dominates corporate CDR and carbon strategy is a competitive liability. Regulatory frameworks will arrive. The question is whether you have built the capability, the relationships, and the supply chain before or after that happens.

Third, the opportunity has moved from volume to structure. Capital is not scarce. What is scarce are the blended financing structures, outcome-based instruments, and insetting models that make long-horizon climate investment compatible with corporate planning cycles. This is where the real opportunity sits.

Companies that act early will be better positioned as regulation tightens and scrutiny increases.

Event details

Final thought

Carbon markets are no longer theoretical. The structures, pathways, and investor appetite are in place. What separates leaders from laggards now is the willingness to build before the policy signals are unambiguous. In Zurich, the message was consistent: the cost of waiting is no longer zero.